Editing a taxonomy by hand can often lead to typographical errors which cause the taxonomy to be invalid. One example of this is a difference between the name of a file and a reference to that file, such as a difference in case. Attempting to point to a file called ‘FILE.xml’ with a URI ending in ‘file.xml’ will fail, meaning that the content of the file is not accessible to other files within the taxonomy and the taxonomy becomes invalid.

Other similar errors include duplicate references (due to copy/paste errors) and undeclared namespace prefixes. These can all be avoided by using certified XBRL software, such as CoreFiling’s Taxonomy Management System, to create the taxonomy. The Taxonomy Management System gives full traceability of all changes made during the taxonomy creation process, as well as creating a taxonomy package valid against the Taxonomy Packages Specification. If an existing taxonomy creation system is in place, the True North validation engine can be used to validate the taxonomy after creation so that any issues can be resolved prior to publication.

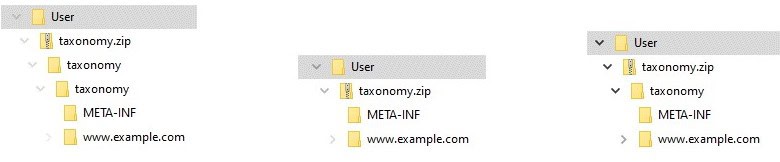

XBRL International recommends that all published taxonomies are provided not only as files on the web, but also as a taxonomy package. The taxonomy package format provides extra information about the taxonomy, such as the entry points used for reporting, in a structured format, and also allows the taxonomy to be quickly installed into compliant software. The most common issue with published taxonomy packages is incorrect directory structure – the package must consist of a zip, containing a single top-level directory with the same name as the zip, with taxonomy files inside that directory, but the top-level directory is often omitted or duplicated by taxonomy publishers.

| Fig 1 – too many directories | Fig 2 – missing directory | Fig 3 – valid structure |

The META-INF directory containing the taxonomy metadata information (taxonomyPackage.xml) and remapping information (catalog.xml) is also a common source of issues – sometimes it is missing or incorrectly placed within the package, and sometimes the files which it should contain are placed elsewhere. Even if the directory contains both a taxonomyPackage.xml and a catalog.xml, errors in their content also crop up, including incorrect ordering of the elements in the taxonomyPackage.xml and remappings to non-XBRL files such as PDFs, as well as typographical errors like the ones mentioned above. Once again, these issues can be detected by simply validating the taxonomy with the True North validation engine prior to publication. XBRL International have produced a handy Practice Profile which explains what a valid package contains.

Best practice issues may not lead to invalid taxonomies, but they can confuse users. Here are some of the top culprits:

| Issue | Why it’s problematic | Example | Solution |

| Shallow remappings | These are likely to overlap with remappings, in other packages or built in to XBRL processing software, and cause conflicts. | Package X depends on Package Y. Both packages include a ‘www.xbrl.org’ directory. Package X uses a file located at www.xbrl.org/files/a/file_a.xsd and package Y uses a file located at www.xbrl.org/files/b/file_b.xsd. Both packages remap ‘http://www.xbrl.org’ to ‘../www.xbrl.org’. XBRL processors don’t know which remapping to use. | Make remappings deep enough to be unique (e.g. Package X should only remap ‘www.xbrl.org/files/a’ and Package Y should only remap ‘www.xbrl.org/files/b’) |

| References to outdated supporting packages, specifications or registries. | Older versions may contain bugs or not support all of the latest taxonomy features. | Use of old namespace xmlns=” http://xbrl.org/PR/2017-02-08/extensible-enumerations-1.1″ which is for an obsolete version of the Extensible Enumerations specification. | Always refer to the latest version of supporting taxonomies, e.g. from https://specifications.xbrl.org/spec-group-index-registries.html |

| Inclusion of non-XBRL files | This makes the taxonomy larger than it needs to be, which can increase memory requirements for processors. | Word/Excel/PDF documents such as release notes and data point model documentation, or copies of files from another taxonomy which could be added to the processor separately. | Provide supporting documentation in a separate ZIP. Don’t copy files from other taxonomies – refer to them at their normative location instead. |

| Lack of backwards compatibility | This can make it difficult for processors to work with multiple versions of the taxonomy. | Version 2.0 of a taxonomy contains some files which are also in version 1.0, and some users need to report using both versions. | Where multiple versions of a taxonomy are valid simultaneously, ensure that their contents do not overlap. |

Hopefully, by following these tips, taxonomy authors can ensure that their taxonomies are consistently high quality every time, ensuring interoperability for everyone’s benefit. Contact us today for more information on the Taxonomy Management System and the True North validation engine.