Following on from our announcement that the True North Data Platform is ready for ESEF, we want to share a little about how our approach to ESEF simplifies and streamlines the user experience.

Around 5,000 issuers across Europe will have to produce annual financial reports in iXBRL format that meet ESMA’s extension and anchoring requirements, within four months of year end. This presents potential challenges in meeting these requirements accurately and on time.

By taking a user-centric, standards-based approach, the CoreFIling solution makes production of ESEF reports business as usual.

Tagging – automate where possible

ESEF involves “tagging” the report by associating financial concepts defined in a technical model of IFRS published by ESMA with specific parts of the human readable text.

![]()

Seahorse® alleviates the manual effort involved through several features that automate much of the process.

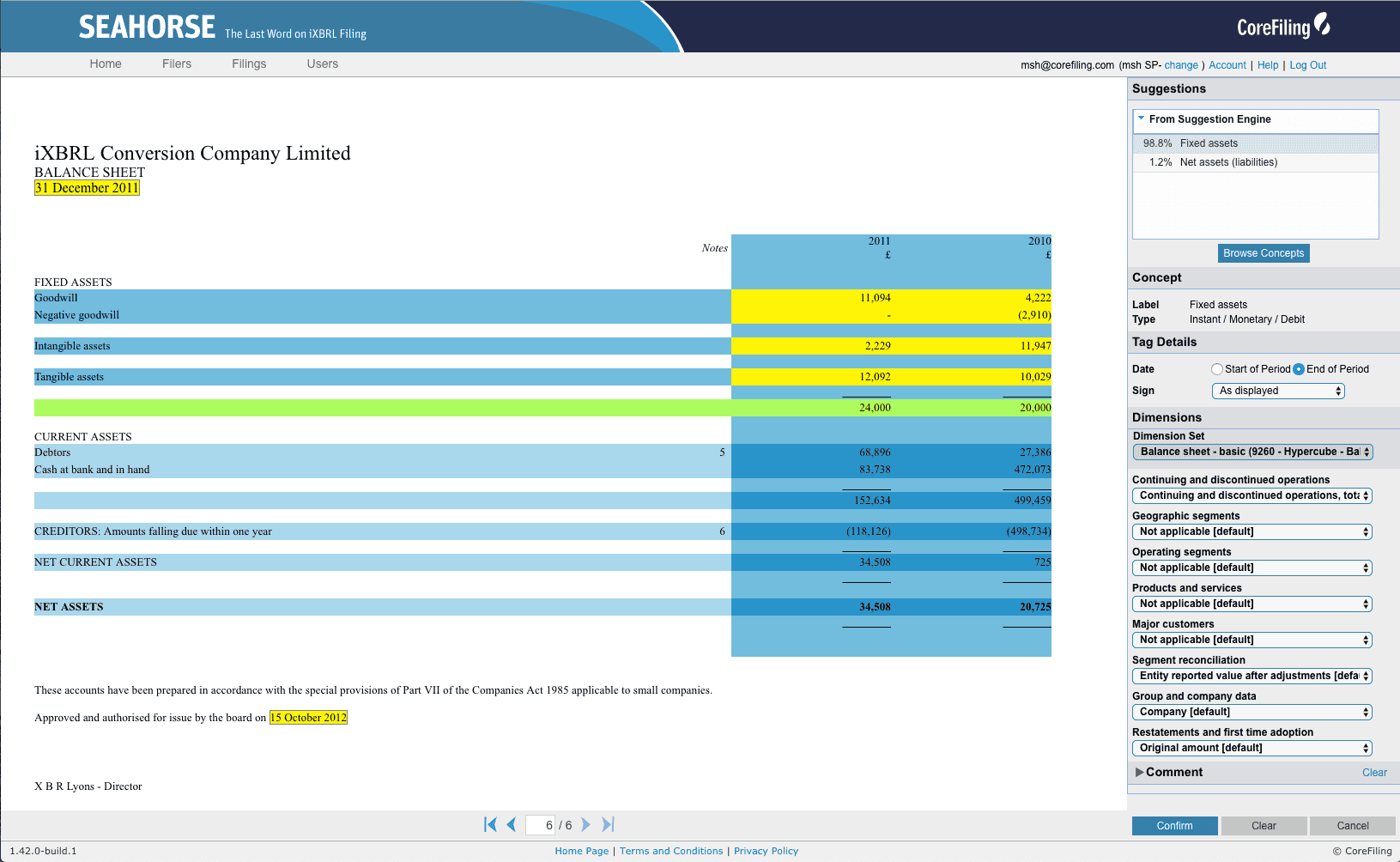

Auto-tagging

The Seahorse® machine learning engine suggests the most appropriate concepts for tagging particular text or tables, but the user remains in control at all times. Our approach is to provide relevant suggestions at the right time, with the level of confidence indicated, and provide the user with time-saving shortcuts so they can make an informed decision.

More about auto-tagging

- The learning engine can be driven by private or shared learning data

- The engine only ever produces suggested, unconfirmed tags, so a human is always responsible for confirming a tag

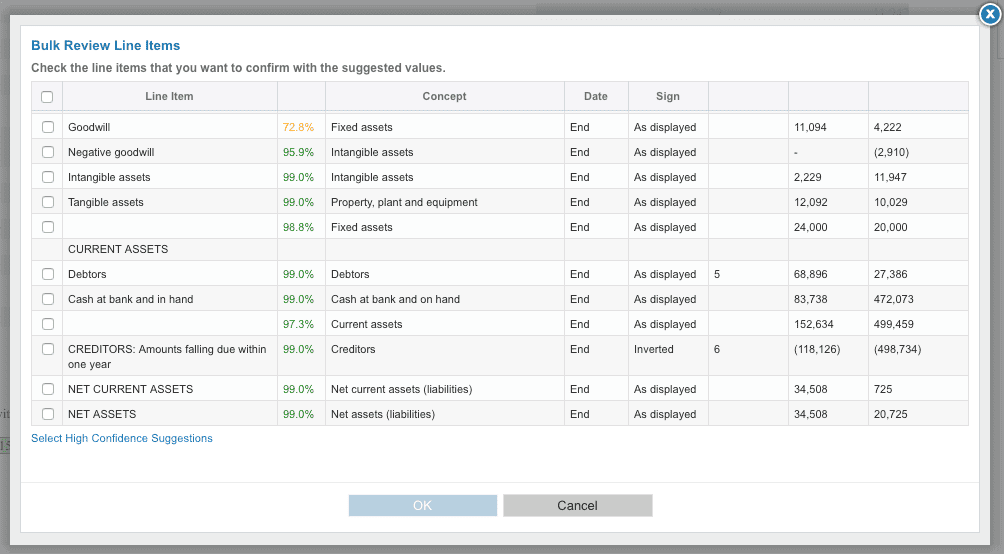

- The confidence level can be used to bulk confirm tags above a confidence threshold

- A specific review workflow is provided to work through any remaining lower confidence items efficiently

Roll-forward

Since filings for sequential years or for entities within the same group are often very similar in structure, Seahorse® can use a previously tagged filing as a guide when tagging the current filing. Our intelligent tag migration engine will recreate tags and associate a level of confidence, so that tagging and review effort can be prioritised appropriately.

Since filings for sequential years or for entities within the same group are often very similar in structure, Seahorse® can use a previously tagged filing as a guide when tagging the current filing. Our intelligent tag migration engine will recreate tags and associate a level of confidence, so that tagging and review effort can be prioritised appropriately.

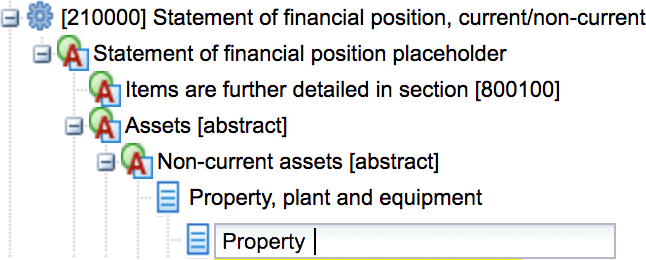

Easily extend taxonomy – as part of the tagging process

Unlike, for example, the UK HMRC mandate, filers can and must create extensions to define their own concepts where “the closest core taxonomy element would misrepresent the accounting meaning of the disclosure being marked up”[2].

Our approach is to treat this as part of the tagging process, by allowing new extension elements to be created in-flow.

![]()

We collect just enough information so that Seahorse® can create all of the required technical artefacts behind the scenes.

More about ESEF's extension requirements

Once the decision to extend has been made, you must ensure the extension meets several technical criteria ESMA define, specifically that extension elements:

- Be included in an appropriate presentation linkbase hierarchy

- Be included in an appropriate definition linkbase hierarchy

- Be associated with appropriate labels in the

- Have an appropriate type and balance attribute

- Be appropriately anchored to core taxonomy elements

Seahorse® automatically generates artefacts to meet the above criteria, driven by a simple user interface that lets the user focus on accurate tagging.

Available now

ESEF is fully supported on our True North Data Platform. Our Seahorse® and Beacon® applications are available to firms and partners now for preparation and review of ESEF filings.

Seahorse® and Beacon® are browser based applications, delivered as SaaS, so clients can get started immediately. Our True North Data Platform also provides a range of APIs, so we can work with you to integrate our capabilities into your own solutions should that be more desirable longer term.

We expect some finer details to be clarified throughout 2019 and 2020 as national regulators, tagging service providers and filers grapple with the new mandate, and we are ready to help our clients keep up with that evolving landscape.

To find out more and request a demo, please visit our ESEF iXBRL landing page.